🌴 Top Retirement Communities in Volusia & Flagler Counties: A Sunshine State Guide 🏡🕶️

Thinking about retiring to Florida? ☀️ You’re not alone! Volusia and Flagler Counties are two of the most sought-after areas on Florida’s east coast for active adults 55 and older. With year-round sunshine, miles of beautiful beaches, and a laid-back lifestyle, it’s easy to see why retirees are flocking here.

As a local real estate professional based in New Smyrna Beach, I often help people from out of state find the perfect retirement community that fits their lifestyle. Here’s a look at some of the most popular 55+ and active adult communities in the region—based on publicly available info and third-party rankings.

📍 Why Retire in Volusia or Flagler County?

🏖️ Beach Access – Miles of scenic coastline, including New Smyrna Beach, Daytona Beach, and Flagler Beach.

🌞 Great Weather – Warm winters and over 200 sunny days per year.

💸 Tax Benefits – Florida has no state income tax and several homestead tax exemptions.

🏥 Healthcare Access – Multiple hospitals and healthcare centers within driving distance.

⛳ Active Lifestyles – Golf, boating, fitness centers, walking trails, and endless community events.

Whether you’re looking for coastal charm, resort-style amenities, or a quiet, low-maintenance lifestyle, Volusia and Flagler Counties offer something for everyone. From vibrant 55+ communities like Latitude Margaritaville to peaceful retreats like Plantation Oaks, the options are diverse—and the sunshine is always included. ☀️

Thinking about making the move? I’d love to help you explore homes in these amazing communities and answer any questions about relocating to this area. 🏡

🎓 Discovering Education in Volusia County: A Guide for New Residents 🏡🌴

If you’re planning a move to Volusia County, Florida, it’s natural to want to understand the area’s educational landscape. While real estate professionals like myself can’t advise on which schools are “best,” I can certainly help you explore objective data and point you to reputable third-party resources that families often use when making decisions. 🧭✨

As someone who personally attended Coronado Beach Elementary, New Smyrna Beach Middle School, and New Smyrna Beach High School, I always encourage new residents to do their own research and visit schools when possible. Below is a factual overview of Volusia County Schools and links to resources where you can learn more. 📊

🏫 Volusia County Schools Overview

Volusia County Schools is the 14th largest school district in Florida, serving more than 63,000 students across 85 schools, including elementary, middle, and high schools, as well as specialized programs. The district is also the county’s largest employer, with over 8,000 staff members, more than half of whom hold advanced degrees. (Source)

In the most recent Florida Department of Education reports, Volusia County Schools maintained a “B” grade, with a significant percentage of its schools rated “A” or “B.” (Source)

🔍 Where to Find School Ratings and Information

Rather than giving personal opinions on schools—which could violate Fair Housing guidelines—I recommend these trusted resources to compare schools based on academic performance, testing data, student-teacher ratios, curriculum offerings, and more:

📌 Examples of Schools Recognized in Public Rankings

Here are a few schools that have received positive rankings or designations in publicly available reports. These examples are meant to showcase the diversity of academic programs and opportunities in Volusia County—not to imply preference or value judgments.

Coronado Beach Elementary (New Smyrna Beach) – Rated 9/10 by GreatSchools.org for test scores and academic progress.

Sweetwater Elementary (Port Orange) – Receives high marks for academic achievement and parent satisfaction.

Spruce Creek High School (Port Orange) – Offers the International Baccalaureate (IB) program and has been recognized in Newsweek’s Top 100 High Schools in past years.

Seabreeze High School (Daytona Beach) – Noted for its well-rounded curriculum and student engagement programs.

Burns Science & Technology Charter School (Oak Hill) – Specializes in STEM education and is often highlighted for its project-based learning approach.

📌 Please note: Ratings may change from year to year, and it’s best to consult the official school websites or speak directly with the school district for up-to-date details.

🧡 My Local Connection

As a local real estate professional and graduate of New Smyrna Beach area schools, I love helping new families explore what makes this community special. While I can’t guide you to a specific school, I’m always happy to provide tools and local insights to support your decision-making process. 🤝

If you’re considering moving to New Smyrna Beach, Port Orange, or anywhere in Volusia County, I’d love to connect and help you get familiar with the neighborhoods, resources, and opportunities in our beautiful coastal region. 🌊🏖️

📲 Explore & Learn More

For the most accurate and up-to-date information about Volusia County Schools, visit:

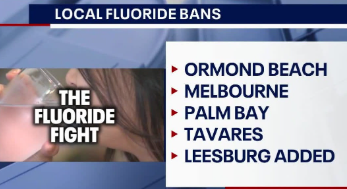

Hey neighbors! There’s been quite a buzz around town lately. Both New Smyrna Beach and Ormond Beach have decided to stop adding fluoride to our water. As a local realtor who cares about our community, I wanted to break it down in a fun and easy-to-read way.

So, What’s the Scoop?

On February 24, the New Smyrna Beach Utilities Commission voted to end water fluoridation. The main reasons? Outdated equipment—replacement costs are nearly $500,000—and ongoing labor and testing fees of about $5,000 per year. Not too long ago, in January, the Ormond Beach City Commission also voted unanimously to stop the process, following concerns raised by local residents and fresh public health perspectives.

Why the Change? 💡

This move lines up with advice from Florida Surgeon General Joseph Ladapo, who, in November 2024, called the continued use of fluoride “public health malpractice.” A report from the U.S. Department of Health and Human Services’ National Toxicity Program hinted at a link between higher fluoride levels and lower IQ in children. Even though top organizations like the American Dental Association and the CDC still support fluoridation for its dental benefits, many are now rethinking the balance between cost, safety, and personal choice.

A Trend Across Florida 🌴

New Smyrna Beach and Ormond Beach aren’t the only ones making waves. Cities like Melbourne, Naples, Tavares, Stuart and Port St. Lucie have also joined the movement. More municipalities are weighing the pros and cons and deciding to let residents choose for themselves.

What’s Your Take?

I’d love to hear from you! Do you see this as a win for personal choice and cost-saving, or are you concerned about missing out on the dental benefits of fluoride? As we see these changes across Florida, it’s a great time for us to chat about what’s best for our community.

Feel free to drop a comment below or send me a topic you’d like to hear about next. I’m here to keep you informed and make sure our community stays ahead of the curve—because, after all, this is our neighborhood!

If you’re a Florida Power & Light (FPL) customer, you may need to brace yourself—a significant rate hike could be coming your way. FPL, Florida’s largest public utility company, is proposing a 14% rate increase, which could add $20 or more to your monthly bill starting in January 2026.

Why Is FPL Raising Rates?

FPL states that this increase is necessary to keep up with Florida’s growing energy demand. With the state’s rapid population boom—275,000 new customers since 2021 and an estimated 335,000 more by 2029—FPL says it must invest in new power generation, including solar energy expansion and infrastructure upgrades.

Is This Justified or Corporate Greed?

Consumer and environmental advocacy groups are pushing back, calling the proposed increase “egregious.” Many are questioning whether this hike is truly for necessary improvements or if it’s simply another way for FPL to boost corporate profits at the expense of Florida residents.

The Hidden Costs You’re Already Paying

If that wasn’t enough, FPL customers are still paying a temporary storm surcharge due to damage from hurricanes Idalia and Debby. This added $12 per month to the average residential bill starting in January 2024, and it could remain in place through the end of the year.

One of the Largest Increases in U.S. History

If this proposed rate hike gets approved, it would be one of the largest in U.S. history. With rising costs of living already impacting many Floridians, this increase could put additional financial strain on households and businesses alike.

How to See the Impact on Your Bill

If you’re wondering how this rate increase could affect you personally, FPL has a calculator tool where you can input your usage and get an estimate of your new bill. It’s worth checking out to see how much more you could be paying if this proposal goes through.

What’s Next?

The decision is now in the hands of state regulators, and public hearings are expected soon. Until then, it’s important to stay informed and engaged in the conversation.

What Do You Think?

Do you believe this rate hike is necessary to support Florida’s growth, or do you think it’s too much for residents to handle? Let us know your thoughts in the comments below, and be sure to stay tuned for more updates on this important issue.

Need Expert Real Estate Advice in Florida?

If you’re thinking about buying or selling a home, having a real estate expert who understands the market is essential. I’m Ryan Tesnow, a dedicated realtor with Coldwell Banker in New Smyrna Beach. Whether you’re looking for your dream home or trying to get the best price for your property, I’m here to guide you every step of the way.

Hello, Florida residents! There’s been a lot of buzz lately about the possibility of eliminating property taxes in our state. Governor Ron DeSantis has expressed support for this idea, stating, “Is it your property or not? You’re basically paying rent to the government to live on your own property.”

How Could This Work?

Eliminating property taxes would require a monumental shift in our tax system. Estimates suggest that Florida would need to find an additional $43 billion to maintain current public services without property tax revenue.

This could mean significant increases in sales taxes or other forms of taxation. For instance, experts warn that replacing the $40 billion loss could require doubling the sales tax, impacting everyday Floridians.

Legislative Actions Underway

To explore this concept further, Senator Jonathan Martin has filed Senate Bill 852, which proposes a study on eliminating property taxes and replacing the revenue with sales tax increases and budget cuts. However, it’s important to note that a similar bill failed to advance last year, and it’s uncertain whether this new proposal will gain traction.

Additionally, Senate Bill 1016, sponsored by Senator Blaise Ingoglia, aims to increase the homestead exemption from $25,000 to $75,000. If approved, this measure would appear on the 2026 ballot and, if passed by voters, take effect in January 2027.

Potential Impact

Eliminating property taxes could have significant implications for local governments, which heavily rely on this revenue to fund essential services like police, fire departments, schools, and infrastructure. Without this funding, services could be reduced, or alternative revenue sources would need to be identified. Some experts view the proposal as a “risky proposition,” suggesting that it could weaken local governments by removing a primary revenue source.

One major concern is school funding. Currently, property taxes contribute significantly to public education budgets. If property taxes were eliminated or reduced, lawmakers would need to find alternative funding sources to ensure that schools receive adequate support. Possible solutions could include increased state funding, reallocating other tax revenues, or raising sales taxes. However, the impact on school quality and resources remains uncertain.

Looking Ahead

As the 2025 legislative session unfolds, it’s crucial to stay informed about these developments. While the complete elimination of property taxes may be ambitious, discussions around tax reform are ongoing. For instance, House Joint Resolution 1257 proposes a constitutional amendment to provide property tax benefits for certain residential properties subject to long-term leases, aiming to extend homestead exemptions to these properties.

Conclusion

The debate over property tax elimination in Florida is complex, involving potential shifts in taxation, funding for public services, and constitutional considerations. As discussions progress, it’s essential for residents to engage with the legislative process, understand the potential impacts, and voice their opinions to ensure that any changes serve the best interests of all Floridians.

Thoughts?

What do you think about eliminating property taxes in Florida? Would the benefits outweigh the potential downsides? Let me know in the comments! If you have any real estate questions or are looking to buy or sell in Florida, feel free to reach out.

Ryan Tesnow, MPA Realtor • Coldwell Banker 394-B N. Causeway | New Smyrna Beach, FL, 32169 Office: (386) 427-3602 | Cell: (254) 206-5020

Mortgage costs stayed stubbornly high in 2024, with 30-year fixed rates holding well above 6% for most of the year. Unfortunately for buyers, 2025 isn’t looking much better.

The Federal Reserve has been cutting interest rates, making the cost of borrowing for loans, credit cards, and auto financing cheaper. But mortgage rates haven’t really budged, frustrating potential buyers who had been holding out for lower home financing costs.

Instead, mortgage rates track more closely with 10-year Treasury bond yields, which lenders use as a benchmark for setting long-term borrowing costs. These yields remain high due to lingering concerns about inflation.

What Mortgage Rates Will Look Like in 2025

With so much economic uncertainty, the outlook for mortgage rates in 2025 remains challenging for buyers.

While the Federal Reserve is expected to further reduce its benchmark interest rate by another 50 basis points, bringing it to a range of 3.75% to 4%, these cuts might not be enough to significantly lower borrowing costs for homebuyers.

That said, most forecasts have 30-year rates below the current rate of 7.11% as of Monday morning, according to Mortgage News Daily.

Here’s a look at the latest projections for 30-year fixed mortgage rates in 2025 from leading financial institutions and industry organizations:

✨ Mortgage Bankers Association forecasts a range of 6.4% to 6.6%

✨ Realtor.com anticipates rates to end the year at around 6.2%

✨ Fannie Mae expects rates to average 6.4% for the year

✨ Wells Fargo projects a slight decline, with rates averaging around 6.3% by the end of the year

✨ Goldman Sachs predicts rates will remain above 6% through 2025

What You Can Do to Lower Your Rate

Despite the high-rate environment, there are strategies to help you secure a better mortgage rate:

2/1 Buydown: This negotiated option allows you to lower your interest rate for the first two years of the loan, giving you some breathing room as you adjust to your new home expenses.

Shop Around for Lenders: Not all lenders offer the same rates. Taking the time to get multiple quotes can save you thousands of dollars over the life of your loan.

Consider Points: Buying down your rate by paying points upfront can reduce your monthly payment significantly.

Improve Your Credit: A higher credit score can qualify you for better rates. Work on reducing debts and paying bills on time to improve your score before applying.

Adjust Your Loan Term: Shorter loan terms, like 15 years instead of 30, often come with lower interest rates.

Stay Informed and Prepared

While we can’t control mortgage rates, being informed and proactive can help you navigate the market. Reach out to a trusted lender or financial advisor to explore your options and create a plan that fits your budget and long-term goals.

⏳ Ready to take the next step? Let’s chat about your homeownership goals and find the best strategy for you!

Understanding the Homestead Exemption in Volusia County

Are you a Florida homeowner? If you’re living in Volusia County and your home is your permanent residence, you could save big on your property taxes through the Homestead Exemption. Let’s break it down so you can take advantage of these savings!

For more information and to apply, visit the Volusia County Property Appraiser’s website:Homestead Exemption

What Is the Homestead Exemption?

The Homestead Exemption is a property tax benefit available to Florida residents who own and occupy their home as their primary residence. This exemption reduces the taxable value of your home, which lowers your annual property tax bill.

Here’s how it works:

Initial $25,000 Exemption: The first $25,000 of your home’s assessed value is exempt from property taxes, including school district levies.

Additional $25,000 Exemption: If your home’s assessed value exceeds $50,000, you qualify for an additional exemption up to $25,000. This applies to all taxes except school district levies. For example, if your assessed value is $75,000 or more, you’ll receive the full additional $25,000 exemption. If it’s less, the exemption is prorated accordingly.

Eligibility Requirements

To qualify for the Homestead Exemption, you must:

Have legal or beneficial title to the property.

Reside on the property as your permanent residence by January 1 of the year for which you are applying.

Apply by March 1 of the same year.

Example of Tax Savings

Let’s say your home has an assessed value of $100,000. With the Homestead Exemption, here’s how your taxable value would be calculated:

Initial $25,000 Exemption: Reduces your taxable value to $75,000.

Additional $25,000 Exemption: Reduces your taxable value further to $50,000 (excluding school levies).

This means you’re only taxed on $50,000 of your home’s value, saving you hundreds of dollars each year!

How to Apply

Homeowners in Volusia County can apply for the Homestead Exemption through the Volusia County Property Appraiser’s Office. If you purchase your home after January 1, you can pre-file your application for the following year. Applications must be submitted by March 1 to qualify for that tax year.

Don’t Miss Out on This Valuable Benefit!

The Homestead Exemption is a powerful way to reduce your property taxes and keep more money in your pocket. Be sure to apply before the deadline to start saving!

For more information and to apply, visit the Volusia County Property Appraiser’s website:Homestead Exemption

As a realtor, I understand how challenging the current housing market can feel, especially with high mortgage rates and rising home prices. But here’s the good news: even in tough markets, there are strategies we can use to help you achieve your dream of homeownership. Let’s take a look at what 2025 might bring and how I can assist you along the way.

What’s Ahead for 2025? 🔮

While mortgage rates might dip slightly, experts predict they’ll remain in the high 6% range. Home prices are expected to continue rising, but at a slower pace—Goldman Sachs forecasts a 4.4% increase, slightly down from 2024’s 4.5%.

This means that while affordability challenges will persist, we have opportunities to navigate this market successfully. With a little creativity and some smart strategies, I’ll help you overcome these hurdles.

How I Can Help You Buy in 2025 💼

Negotiate Closing Cost Assistance 💵

Closing costs can add up quickly, but I’ll work to negotiate with sellers for closing cost contributions. This can save you thousands and make your home purchase more affordable upfront.

Down Payment Assistance (DPA) Programs 🤝

Many buyers think they need 20% down, but there are programs available to help with much smaller down payments—even as low as 3% or less. I’ll guide you to grants, loans, and other assistance programs that fit your needs.

Rate Buydowns 💰

High mortgage rates? No problem! I can negotiate rate buydowns, where either the seller or lender helps cover part of your interest rate for the first year or two, easing your monthly payment. This is especially helpful as you adjust to homeownership costs.

Explore First-Time Homebuyer Incentives 🏠

From tax credits to reduced fees, there are numerous incentives available to first-time homebuyers. I’ll ensure you’re aware of every benefit you qualify for.

Identify Homes with Builder Incentives 🏗️

If you’re considering new construction, I’ll help you find builders offering perks like appliance packages, closing cost coverage, or rate lock incentives. These can add significant value to your purchase.

Connect You with Trusted Lenders 📋

The right lender makes all the difference. I’ll connect you with lenders who specialize in affordable loans and competitive interest rates. Together, we’ll find a loan product that fits your budget.

Why Work with Me? 🙋♂️

Navigating today’s market can be tricky, but you don’t have to do it alone. As your realtor, I’ll:

Stay on Top of Market Trends: Providing up-to-date information on rates, prices, and local market conditions.

Offer Personalized Solutions: Every buyer is different, and I’ll tailor my approach to meet your unique needs.

Be Your Advocate: From negotiating terms to ensuring a smooth closing, I’ll fight for your best interests every step of the way.

Ready to Make Your Move in 2025? 🚪✨

Don’t let the market intimidate you—let’s make a plan together! Whether it’s finding a home, securing financial assistance, or negotiating the best deal, I’m here to help.

📲 Reach out today to start your homeownership journey! #YourRealtor #HomeBuyingMadeEasy #DreamHome2025

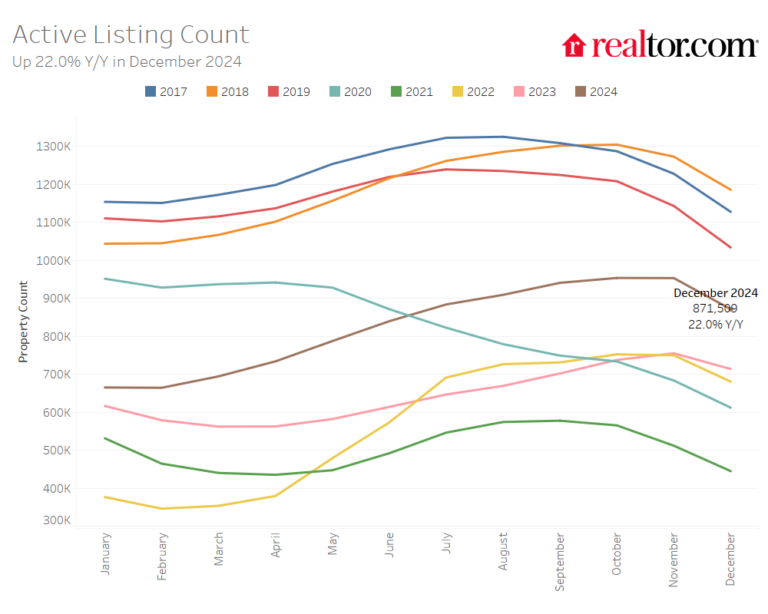

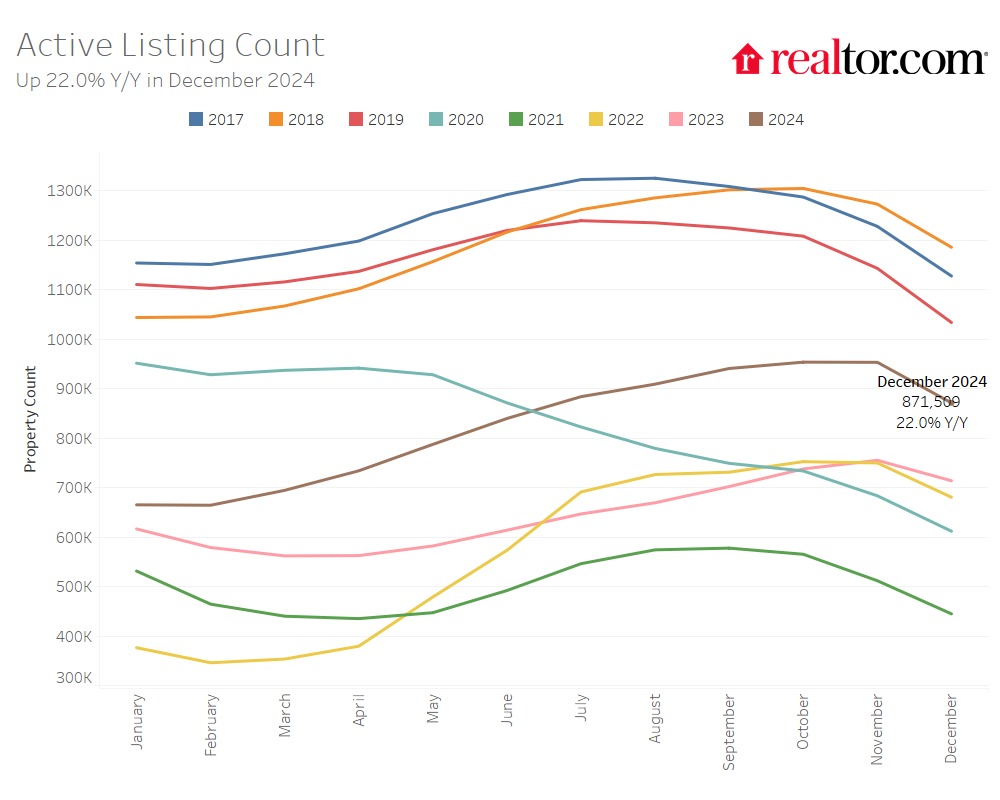

The number of homes actively for sale continues to be higher compared with last year, growing by 22%, a 14th straight month of growth, but due to seasonality have plummeted to their lowest level since June.

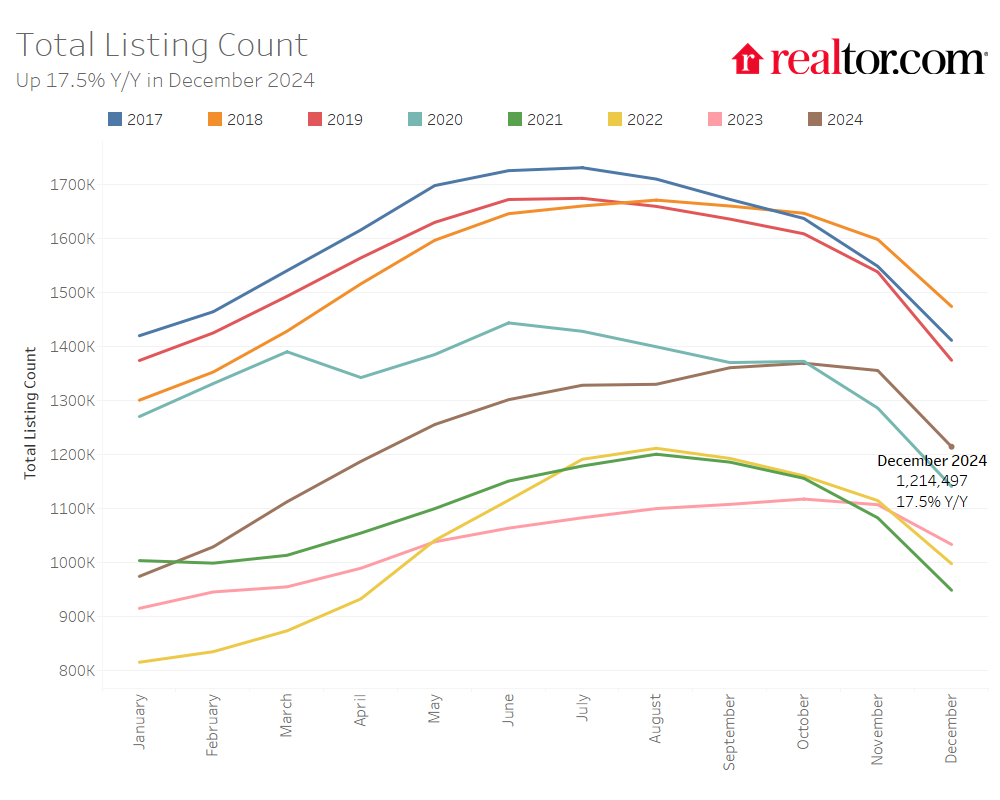

The total number of unsold homes, including homes that are under contract, increased by 17.5% compared with last year.

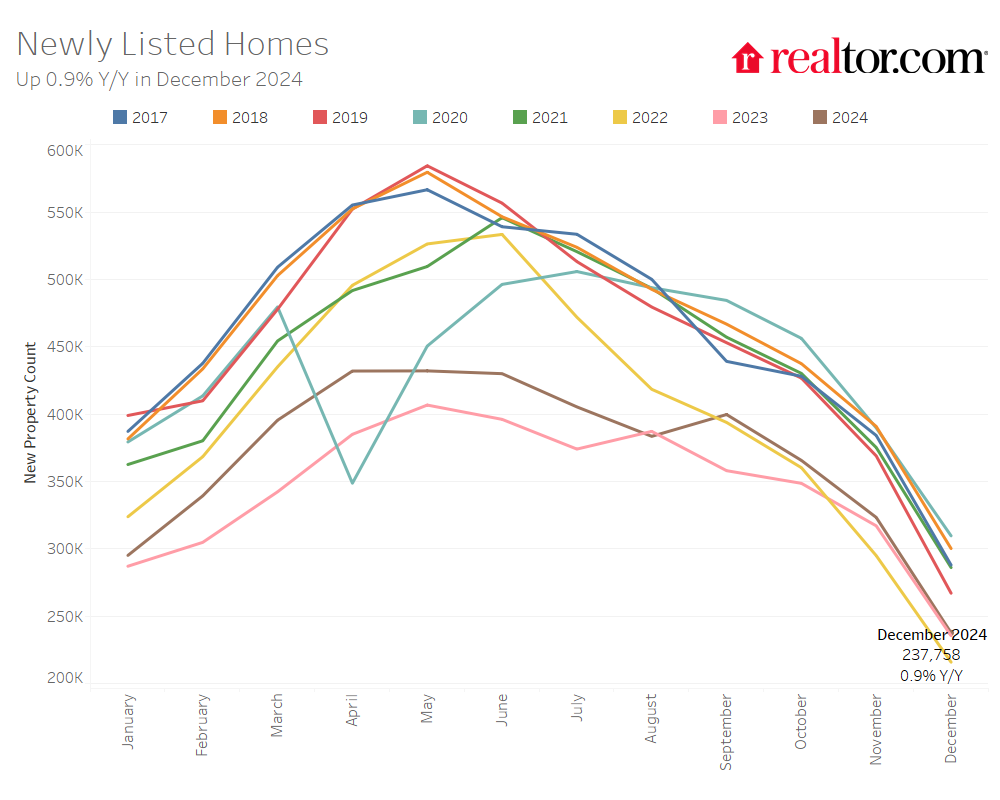

Home sellers slowed down their activity slightly in December, with just 0.9% more homes newly listed on the market compared with last year, down from 2% last month.

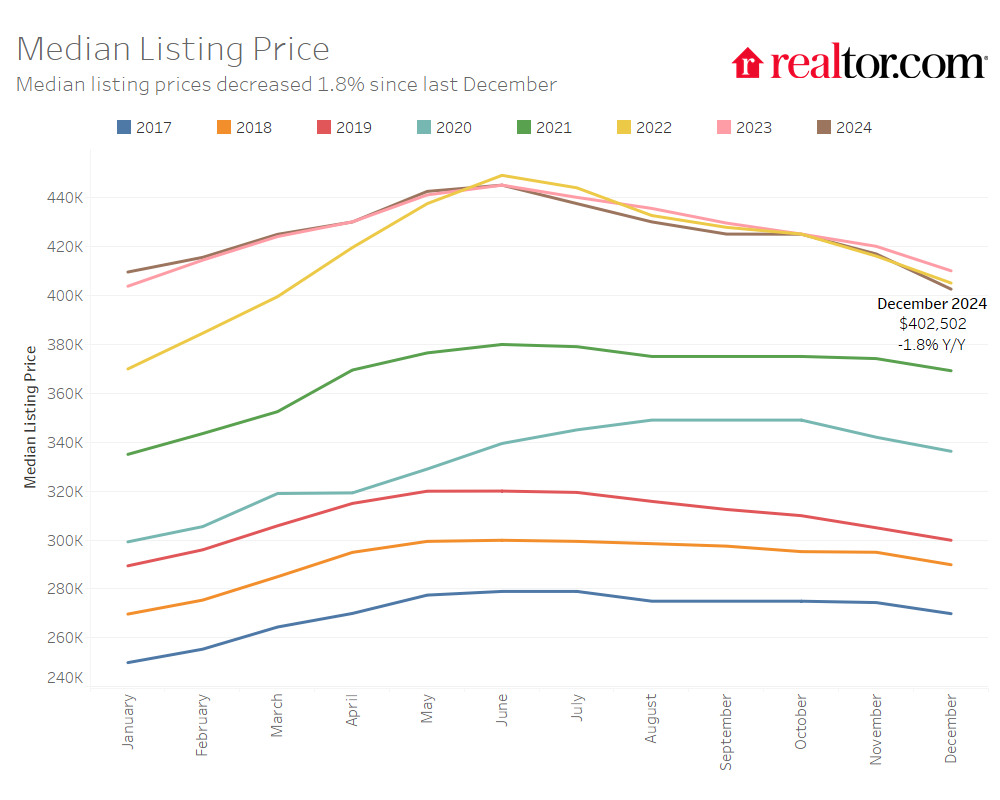

The median price of homes for sale this December was down 1.8% compared with last year, at $402,502. However, the median price per square foot grew by 1.3%, indicating that the inventory of smaller and more affordable homes continues to grow in share.

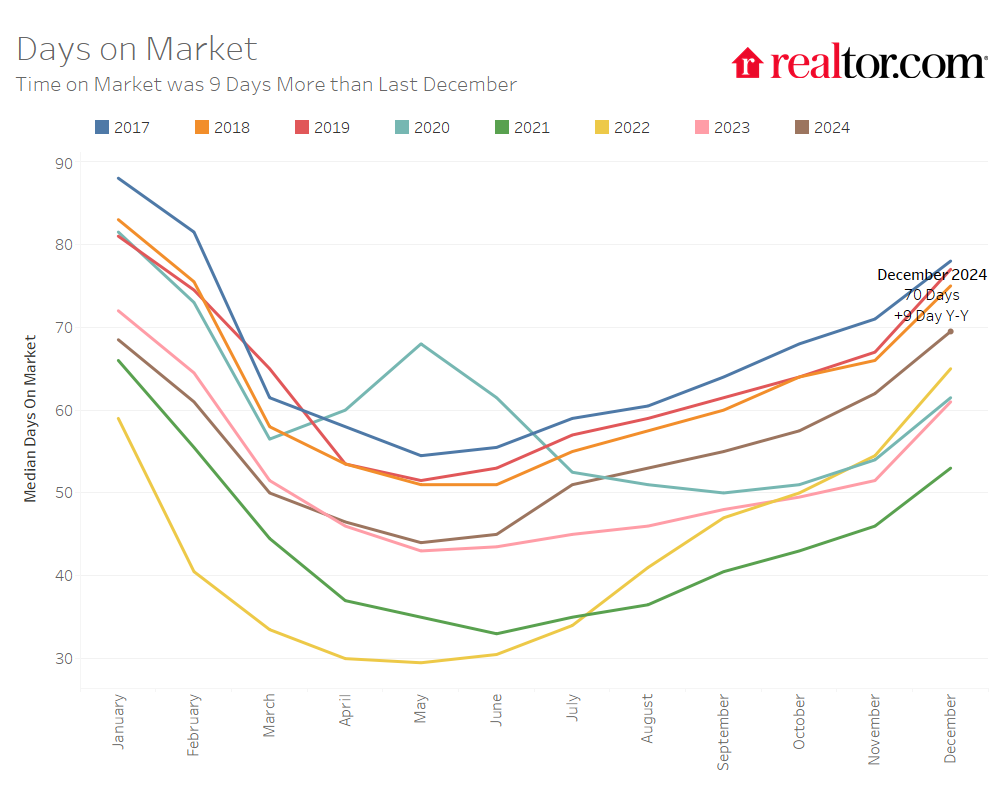

Homes spent 70 days on the market, the slowest December in five years and the slowest month since January 2023. This is nine more days than last year and eight more days than last month.

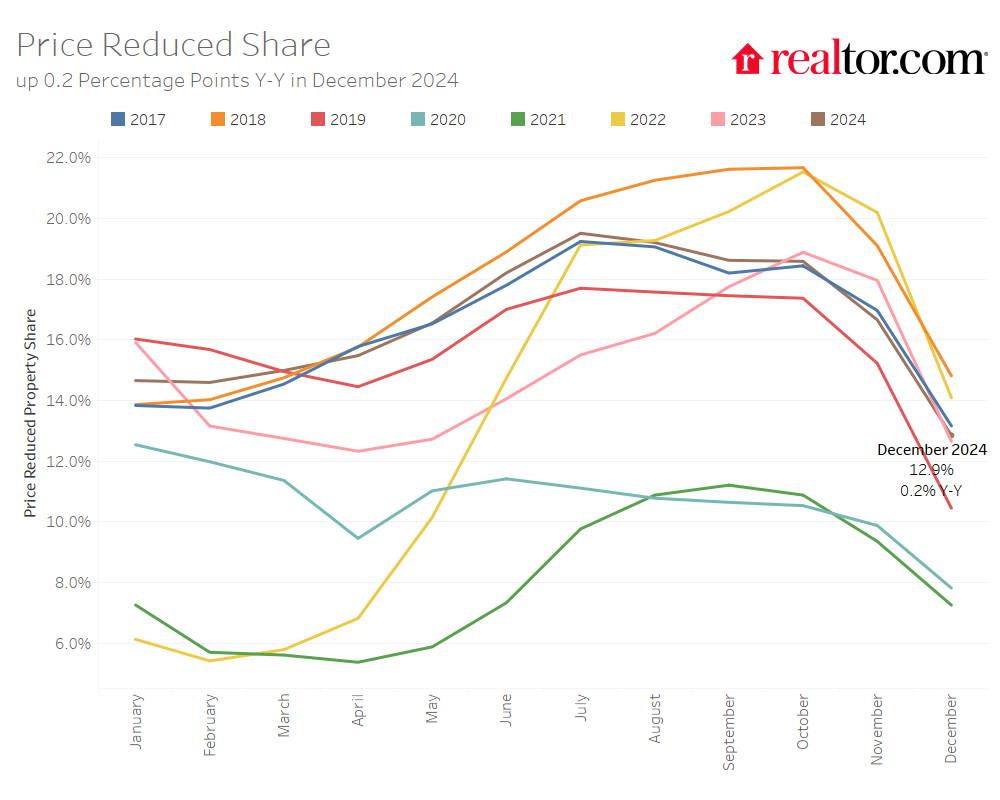

The share of listings with price cuts was essentially flat from last year, with 12.9% of sellers cutting prices in December, up slightly from 12.7% in December 2023.

The total number of homes for sale, including homes that were under contract but not yet sold, increased by 17.5% compared with last year, growing on an annual basis for the 12th month in a row. This is down from 22.5% last month.

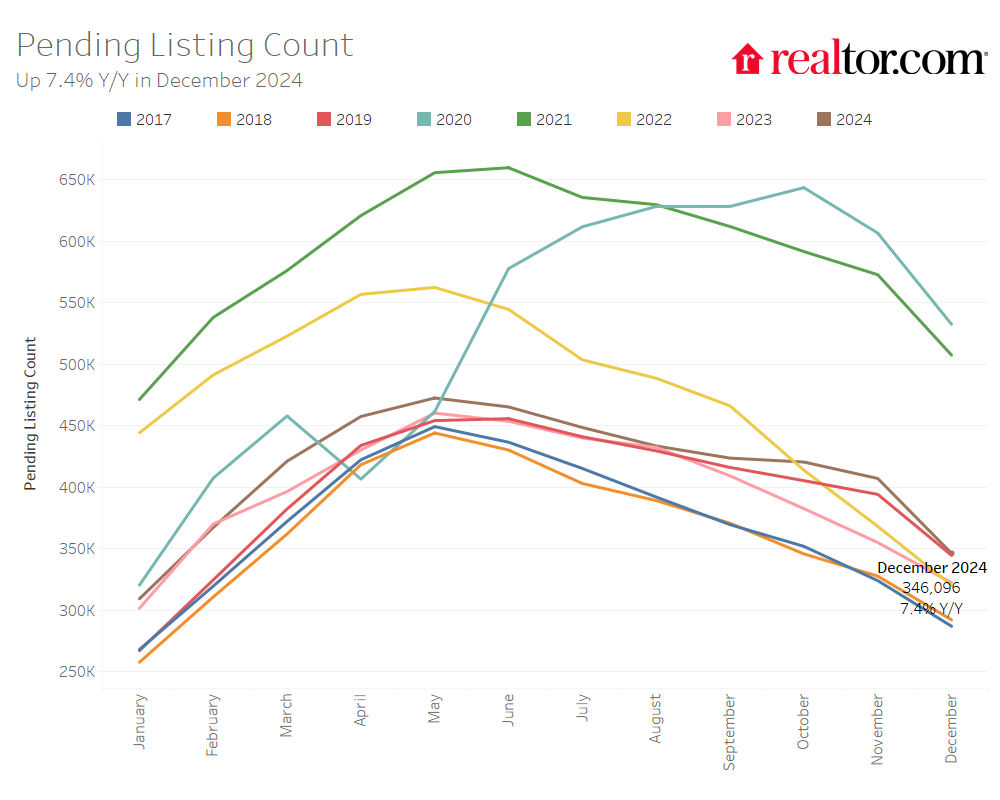

The number of homes under contract but not yet sold (pending listings) continued to rebound in December, increasing by 7.4% compared with last year, just under 50% less than November’s 14.7% gain. This slowdown is at least partly due to mortgage rates in November and December that were approximately 40–50 basis points higher than in September and October. Though rates are significantly higher today than they were just a few months ago, our 2025 forecast shows that as both lower rates and time chisel away at the “lock-in” effect that has held back sales this year, we should expect home sales to rise modestly by 1.5% in 2025.

Sellers slightly increased their activity this December as newly listed homes were just 0.9% above last year’s levels, a decrease from November’s rise of 2%. We noted last month that the sharp decrease in mortgage rates in mid-August could lead to an increase in listings in the coming months as lower rates begin to entice the marginal homeowner to sell, and that’s exactly what happened in September and October. But with higher rates taking a bite out of homebuying power, fewer new sellers are coming to the market this winter compared with this past fall.

Regional and metro area inventory trends

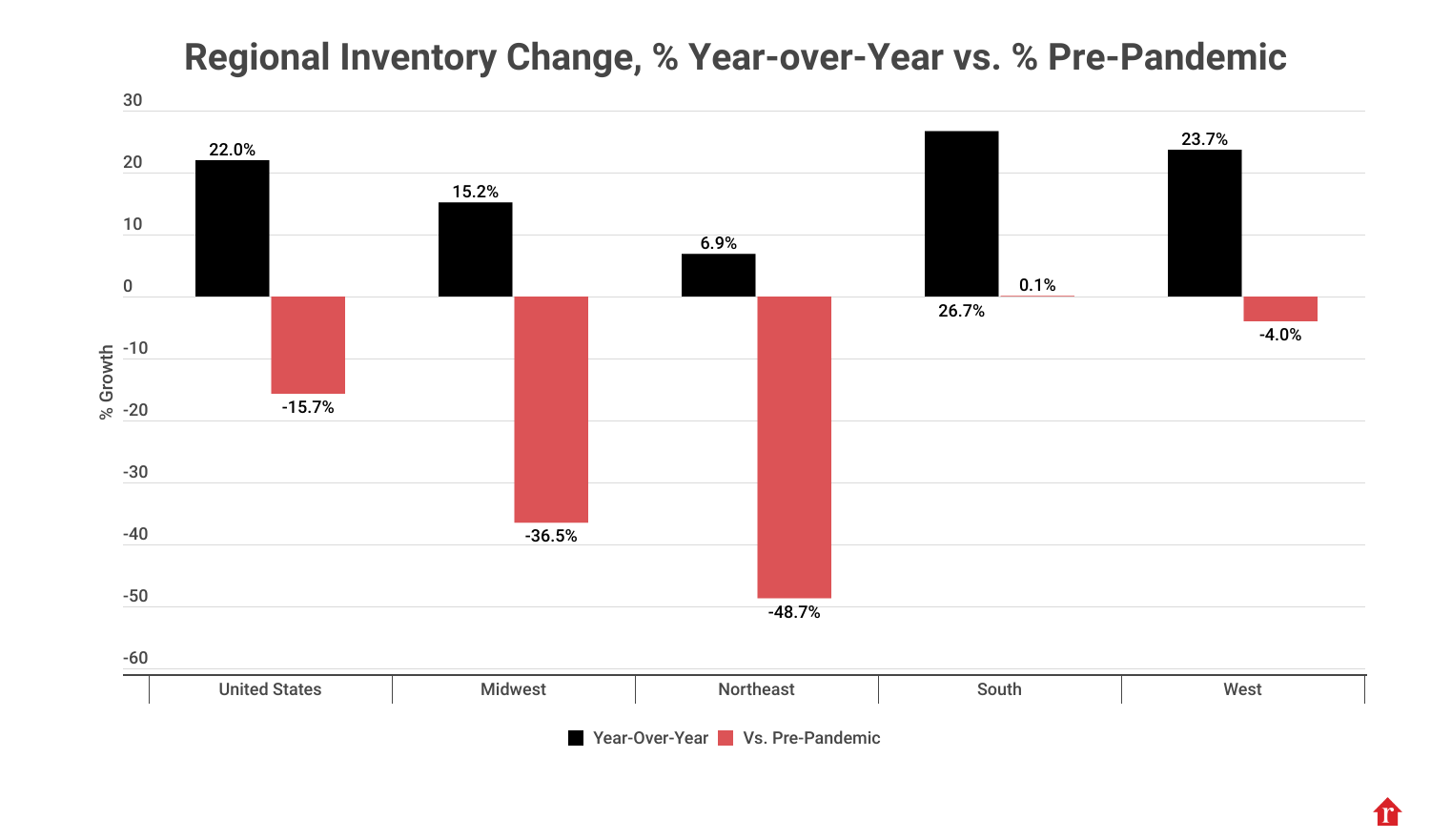

The South and West are closest to bridging the inventory gap

In December, all four regions continued to see active inventory grow over the previous year. The South saw listings grow by 26.7%, while inventory grew by 23.7% in the West, 15.2% in the Midwest, and 6.9% in the Northeast. Compared with the typical December from 2017 to 2019, before the COVID-19 pandemic, the South fully closed the gap in inventory, up 0.1% compared with pre-pandemic levels. Meanwhile, the gap was 4% in the West, and much larger in the Midwest and Northeast, at 36.5% and 48.7%, respectively.

With the exception of San Jose, CA, the inventory of homes for sale increased in all of the largest metros compared with last year. Metros that saw the most inventory growth included Miami (+45.4%), Orlando (+42.4%), and Denver (+41.9%).

Despite higher inventory growth compared with last year, most metros still had a lower level of inventory when compared with pre-pandemic years. Among the 50 largest metro areas, 16 saw higher levels of inventory in December compared with typical 2017 to 2019 levels. This is the same number as last month. The top metros that saw inventory surpass pre-pandemic levels were predominantly in the South and included Memphis (+37.7%), Austin (+36.5%), and Orlando (+34.9%).

The South saw newly listed homes increase the most compared with last year

Newly listed home inventory increased by 4.8% in the South and 2% in the West, while falling by 5.6% in the Northeast and 6.6% in the Midwest. The gap in newly listed homes compared with pre-pandemic 2017 to 2019 levels was also the lowest in the South, where newly listed homes were just 1.6% below pre-pandemic levels. In comparison, they were down 12.4% in the Midwest, 19.7% in the Northeast, and 25.5% in the West.

In December, 22 of the 50 largest metros saw new listings increase over the previous year, down from 32 last month. However, just seven large metros—including Houston, Birmingham, and Miami—saw more newly listed homes this December compared with the typical pace of new listings from December 2017 to 2019. This is up from four large metros in the prior month. The metros that saw the largest growth in newly listed homes compared with last year included Atlanta (+17.8%), Birmingham, (+17.1%), and Virginia Beach (+16.9%).

Homes are spending more time on the market compared with last year, but less than pre-pandemic levels

The typical home spent 70 days on the market this December, which is nine more days than the same time last year and eight more days than last month. This marks the slowest December since 2019 and the slowest month since January 2023, marking the ninth month in a row where homes spent more time on the market compared with the previous year. However, the time a typical home spends on the market is still eight days less than the average December from 2017 to 2019.

Regional and metro area time on the market trends

In the South, where the growth in home inventory has been the largest, the typical home spent 10 more days on the market in December compared with last year. Out West, homes are staying on the market eight days longer. However, in the Midwest and Northeast, homes are staying on the market just four and five more days, respectively, than the same time last year.

While three regions were still seeing time on the market below pre-pandemic levels, homes in the West are now spending one more day on the market compared with the typical December from 2017 to 2019. Time on the market was four days less than pre-pandemic levels in the South, 17 days less in the Midwest, and 19 days less in the Northeast.

Meanwhile, time on the market increased compared with last year in 46 of the 50 largest metro areas this December, up from 42 last month. It increased the most in Nashville (+22 days), Orlando (+21 days), and Rochester (+21 days). Fourteen markets saw homes spend more time on the market than typical 2017 to 2019 pre-pandemic timing, with a few notable standouts: Nashville (+22 days), Orlando (+22 days), and Rochester (+21 days).

The median list price was down slightly from last December, but the price per square foot continues to rise

The national median list price in December was at $402,502, which is about $15,000 lower than last month and 1.8% lower than last December. However, when a change in the mix of inventory toward smaller homes is accounted for, the typical home listed this year has increased in asking price compared with last year. The median listing price per square foot increased by 1.3% in December compared with the same time last year. Moreover, the typical listed home price has grown by 34.2% compared with December 2019, while the price per square foot grew by 49.5%.

The percentage of homes with price reductions was up 0.2% from last year, at 12.9%. What’s more, the overall share of inventory with price cuts is +2.4pp higher than the shares seen between December 2017 and December 2019, up from +1.4pp last month.

Regional and metro area price trends

In December, listing prices were up compared with December 2023 in the Midwest and Northeast, at 0.7% and 0.4%, respectively. Listing prices fell by 1.3% and 2.3% in the West and South. Controlling for the mix of homes on the market by looking at price per square foot, all regions showed greater growth rates of 0.3% to 3.9%. Among large metros, the median list price in Cleveland (+9.1%), Milwaukee (+6.7%), and Detroit (+6.2%) saw the biggest increases.

Meanwhile, all 50 of the largest metropolitan areas have seen sizable price growth compared with homes listed before the pandemic. Compared with December 2019, the price-per-square-foot growth rate in the 50 largest metros ranged from 17.9% to 66.8%. The markets where sellers saw the greatest increase in price per square foot included the Hartford metro area (+66.8% vs. December 2019), New York (+66.8%), and Nashville (+60.3%). Markets that saw the lowest return included San Francisco (+17.9%), San Jose (+24.0%), and New Orleans (+25.5%).

Compared with last year, price reductions were down 0.8 percentage points in the Northeast and 0.4 percentage points in the Midwest, but up 0.1 percentage points in the South and 1.5 percentage points in the West. Of the 50 largest metros, 26 saw the share of price reductions increase compared with last December, up from 11 in November. Denver saw the greatest increase (+11.5 percentage points), followed by Portland, OR (+8.7 percentage points), and Providence (+7.8 percentage points).

🏌️♂️ Best Golf Course Communities in Volusia County 🏡

Looking for the perfect blend of luxury living and top-notch golfing? Volusia County is home to some of the best golf course communities in Florida! Here’s a list of must-see communities, their standout features, and why they’re a golfer’s paradise.

1. Venetian Bay 🌴⛳

Location: New Smyrna Beach

Why It’s Great:

Venetian Bay offers a championship 18-hole golf course and an upscale clubhouse with dining options. Residents enjoy access to a Beach and Swim Club, walking and biking trails, and onsite restaurants. This community combines a vibrant lifestyle with scenic views of lush fairways.

Why It’s Great:

Nestled in a serene setting near Tomoka State Park, Halifax Plantation boasts an 18-hole course surrounded by natural beauty. Amenities include a full-service restaurant, tennis courts, and a fitness center. Perfect for those seeking tranquility and a premier golfing experience.

Why It’s Great:

Home to two world-class golf courses, Hills and Jones, LPGA International offers challenging play for all skill levels. Residents enjoy resort-style amenities, including a luxury clubhouse, pool, and fine dining. Its central location is just minutes from Daytona’s shopping, dining, and beaches.

Why It’s Great:

Sugar Mill is a private, member-owned community with a 27-hole championship golf course designed for serious golfers. The club also features pickleball courts, a fitness center, and dining options. The tight-knit community vibe makes it extra special.

Why It’s Great:

A unique community that blends luxury living with aviation and golf. It features an 18-hole course, a country club, and a private airstrip for aviation enthusiasts. This gated community offers a lifestyle like no other, with plenty of social activities and beautiful homes.

Why It’s Great:

Known for its affordable luxury, Cypress Head features an 18-hole public golf course surrounded by beautiful homes. Residents enjoy a clubhouse, pro shop, and a friendly neighborhood feel, making it ideal for families and retirees alike.

Why It’s Great:

Victoria Hills offers a challenging 18-hole course with scenic views, a fitness center, and community pools. Its charming, family-friendly vibe and proximity to downtown DeLand make it a great choice for those seeking an active lifestyle.

Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link